The Swiss franc soared to a ten-year high, the dominance of the US dollar was challenged, and global capital flooded into gold as a safe haven

- April 14, 2025

- Posted by: Macro Global Markets

- Category: News

The Swiss franc surged to 1.2341 against the US dollar, reaching a new high since the “Black Swan” event in 2015. The US dollar index plummeted 2.1% to 99.8 in a single day, and the three major US stock indexes fell more than 2.5% simultaneously. The S&P 500 triggered a circuit breaker mechanism during trading.

1、 Swiss Franc Rise: A ‘Counterattack’ of Safe haven Currency

The logic behind exchange rate fluctuations

Geophysical risk premium: the sudden coup in Damascus, the Syrian capital, and the Russia-Ukraine conflict continued to stick together, combined with the overall escalation of the Sino US European trade war, the market risk aversion boosted the demand for the Swiss franc as a “safe currency”. According to data from the Swiss National Bank, the trading volume of Swiss francs in the interbank market surged by 380% year-on-year on April 10th.

Policy differentiation: The Swiss National Bank maintains a negative interest rate policy (-0.75%), but supports the local currency by selling foreign exchange reserves (with a daily intervention scale of 12 billion Swiss francs), in sharp contrast to the Federal Reserve’s “protracted high interest rate war”.

Technical breakthrough: The Swiss franc broke through the long-term resistance level of 1.20 against the US dollar after the 2015 “decoupling from the euro” crisis, triggering algorithmic trading to buy along with the trend and further amplify the gains.

market impact

Export enterprises are under pressure: Swiss watch industry (accounting for 12% of total exports) is facing profit margin compression due to the appreciation of the Swiss franc, and Swatch Group’s stock price fell 4.7% in a single day.

Cross border capital flow: Eurozone funds accelerated to flow into Swiss treasury bond, and the yield of 10-year Swiss franc treasury bond fell to -0.35%, a record low.

2、 The collapse of US dollar hegemony: from “trust crisis” to “system reconstruction”

The US dollar has experienced a credit crisis, with the US dollar index experiencing a cumulative decline of 12% this year, the largest annual decline since the collapse of the Bretton Woods system in 1971. IMF data shows that the proportion of global central bank US dollar reserves has decreased from 72% in 1999 to 58%.

Global de dollarization accelerates

Restructuring of settlement system: The transaction volume of the new payment system in BRICS countries has surged by 380% year-on-year, and the pilot of digital RMB cross-border payment has been expanded to 47 countries, covering 65% of global trade volume.

Commodity decoupling: Saudi Arabia accepts RMB settlement for oil, LME plans to launch a metal pricing system based on gold, and 32% of global crude oil trade has achieved non US dollar settlement.

Central Bank Gold Purchase Trend: By 2025, the proportion of global central bank gold reserves will rise to 23%, and the annual gold purchase volume may exceed 1000 tons. The People’s Bank of China increased its gold holdings by 22 tons to 2250 tons in March.

3、 Global Capital Battle Royale: The ‘Faith Shift’ from Stocks and Bonds to Gold

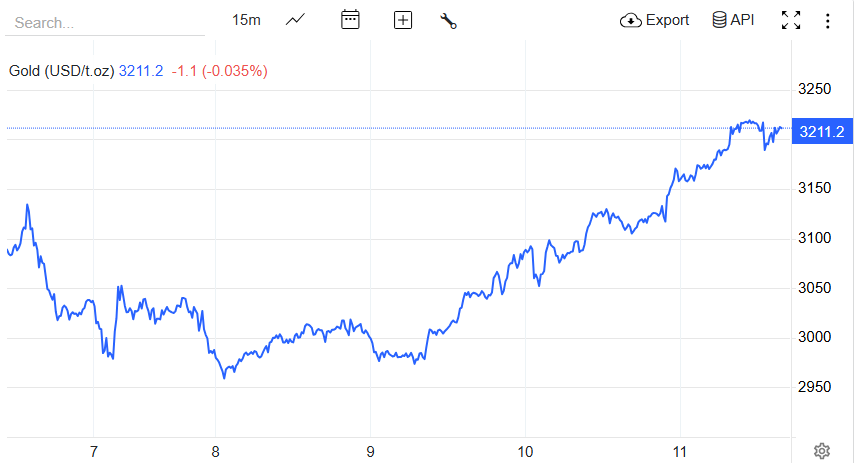

Safe haven asset frenzy: Spot gold broke through $3210/ounce, with a daily increase of 1.33%.

ETF holdings surge: SPDR Gold Trust, the world’s largest gold ETF, saw its holdings surge by 12.62 tons to 949.71 tons, with a daily increase in holdings reaching a new high since 2024.

Risk Warning: Market volatility is influenced by policies and emotions. It is recommended that investors develop strategies based on their own risk tolerance to avoid excessive leverage. The above analysis is for reference only and does not constitute investment advice.