The US dollar plummeted to a three-year low! Multinational US companies launch ‘ultra long defense war’

- April 22, 2025

- Posted by: Macro Global Markets

- Category: News

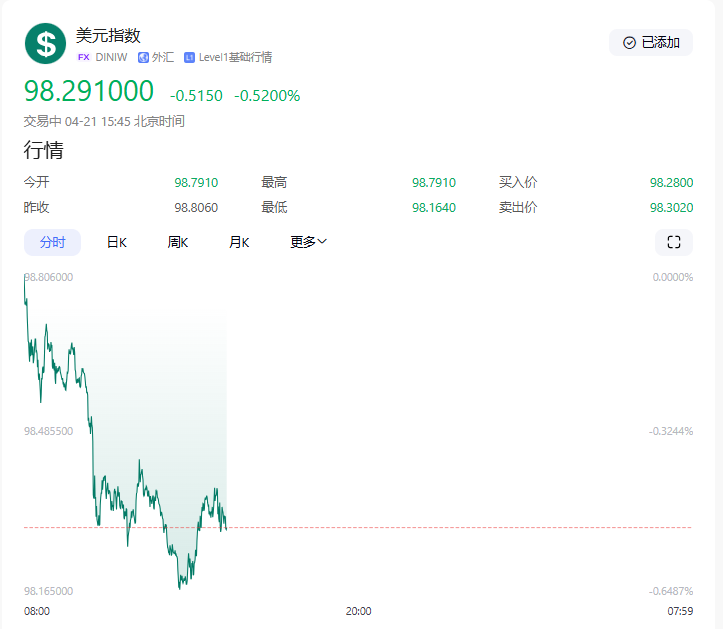

On April 21, 2025, the US dollar index (DXY) continued its downward trend, hitting a intraday low of 98.164, a 1.03% drop from the previous trading day’s closing price, setting a three-year low since April 2022. As a result, the euro/dollar exchange rate soared to 1.1485, the pound/dollar broke through 1.3350, and the yen/dollar strengthened to 141.80 due to expectations of Bank of Japan intervention. Behind this exchange rate storm is the collective launch of a “super long defense war” by multinational American companies – companies such as Apple and Tesla have extended their currency hedging cycle from the usual 3-6 months to 2-5 years, setting a rare record in nearly a decade. The spot gold price has broken through 3390 US dollars per ounce, up 1.68% from the previous day, setting a new historical high. Market concerns about the “US dollar credit crisis” have further intensified.

1、 The multidimensional driving logic behind the sharp decline of the US dollar

The ‘Butterfly Effect’ of the Federal Reserve’s Policy Shift

Market expectations for the Federal Reserve’s interest rate cuts continue to rise, with federal funds rate futures showing a cumulative rate cut of 90 basis points by 2025. Despite Powell’s emphasis on “data dependence” at the FOMC meeting in April, the slowdown in US GDP growth to 1.8% in the first quarter and the year-on-year increase in the core PCE price index to 2.9% have forced investors to reprice US dollar assets. Goldman Sachs’ latest report suggests that the US dollar index may hit the 95 level before the end of the year, hitting a new low since 2018.

The ‘shock wave’ of Trump’s tariff policy

After the US government announced on April 2nd the imposition of a 32% tariff on key areas such as semiconductors and new energy vehicles, the risk of global supply chain restructuring has intensified. The demand for the US dollar as a trade settlement currency has decreased, with data from the Chicago Mercantile Exchange (CME) showing a 12% weekly decrease in open contracts for US dollar futures. What’s even more tricky is that trading partners such as Japan and the European Union have initiated retaliatory tariffs, creating a vicious cycle of ‘tit for tat’.

Global central banks’ ‘de dollarization’ actions

The People’s Bank of China increased its holdings of gold by 29 tons in April, with total reserves exceeding 2292 tons; The Reserve Bank of India announced a reduction in the allocation of US dollar assets from 65% to 58%. This trend of “de dollarization” is particularly evident in emerging markets, where countries such as Brazil and Argentina have included the renminbi in their foreign exchange reserves. The Bank for International Settlements (BIS) report shows that the proportion of the US dollar in global foreign exchange transactions has decreased from 88% in 2022 to 83%.

2、 The ‘ultra long defense war’ of multinational American companies

The ‘Extreme Extension’ of Hedge Strategy

According to data from Mizuho Bank, its corporate clients have generally extended the hedging period of forward contracts from 6 months to 2-5 years, marking the first “ultra long term defense” since the 2008 financial crisis. Apple disclosed in its latest financial report that its foreign exchange hedging scale has reached $42 billion, covering overseas revenue for the next three years. Tesla is locking in profits in the European market before 2027 by purchasing Euro call options.

Geopolitical restructuring of supply chain

General Motors announced a 50% increase in production capacity at its Mexico factory to avoid the impact of fluctuations in the US dollar exchange rate on the North American supply chain; Boeing is accelerating the layout of maintenance centers in Southeast Asia to reduce its reliance on US dollar settlements. According to a survey by Boston Consulting Group (BCG), 68% of multinational corporations plan to complete the “regionalization” adjustment of their supply chains by 2025.

Currency switching in financing channels

Technology giants such as Microsoft and Amazon have turned to the euro bond market for financing, with the issuance of euro denominated corporate bonds reaching 38 billion euros in April, a year-on-year increase of 210%. This strategy of “borrowing low interest currency and earning high interest assets” not only reduces exchange rate risk but also increases the return on investment.

3、 The ‘long short game’ in the foreign exchange market

The ‘critical point’ of central bank intervention

On April 21st, Japanese Finance Minister Katsuyuki Kato issued a rare warning that if the yen exchange rate falls below the 142 mark, he will consider initiating an “emergency intervention”. In 2024, Japan intervened in the market four times, consuming a total of over 15 trillion yen in foreign exchange reserves. At the same time, the European Central Bank announced a 25 basis point interest rate cut on April 18th, pushing the euro dollar exchange rate above 1.14 and further squeezing the space for the US dollar.

Innovative Tools for Enterprise Risk Avoidance

According to data from the London Stock Exchange, the trading volume of foreign exchange options for Eurozone companies increased by 47% in a single week, with “digital options” (only effective in specific exchange rate ranges) accounting for 31%. This tool can not only reduce hedging costs, but also provide “unexpected returns” during severe exchange rate fluctuations.

Structural transformation of capital flow

According to data from the US Treasury Department, foreign investors sold $68 billion worth of US Treasury bonds in March, reaching a new high since 2020. The flow of funds shows polarization: safe haven funds flood into gold ETFs (SPDR gold holdings increase by 19 tons per week), while risk appetite funds flow into emerging market stocks, with the MSCI Emerging Markets Index rising by 3.2% per week.

The continuous decline of the US dollar and the “ultra long defense” of multinational corporations are essentially a microcosm of the restructuring of the global monetary system and supply chain pattern. For investors, they are currently in a triple period of “US dollar depreciation – gold hedging – corporate restructuring”: in the short term, they need to be wary of overbought pullbacks and policy changes, in the medium term, they can allocate gold ETFs and physical gold bars on dips, and in the long term, they need to pay attention to the “time difference” between the global central bank’s gold buying speed and the turning point of the Federal Reserve’s policy.